Manual data entry is error-prone, time-intensive, and risky for modern businesses. Even a single typo can lead to incorrect financial reporting, compliance issues, or missed opportunities. Automated accounting – increasingly powered by AI – reduces these risks by streamlining processes and eliminating repetitive manual tasks.

The hidden dangers of manual accounting

Outdated manual processes still dominate many businesses, often with costly consequences. Research indicates that SMEs lose 120 hours/year per employee due to manual data input, while 92% of routine accounting tasks are automatable. These facts further highlight the great potential automated accounting has to offer.

Dangers of Manual Accounting

Explanation

Increased risk of human error

Typos, missing entries, or incorrect figures can quickly lead to inaccurate financial statements.

Inaccurate time tracking

Without digital tools, time tracking is often based on estimates, which impacts payroll and invoicing.

Time-consuming data entry

Manual entry takes up significant time and distracts from strategic finance tasks.

No real-time data

Data updates are delayed, which makes it hard to make timely, informed business decisions.

Increased risk of fraud

Lack of system controls facilitate unauthorised transactions to go unnoticed.

Increased costs

Manual accounting leads to higher staffing needs, inefficiencies, and a greater risk of costly errors.

Increased risk of human error

Manual processes are prone to mistakes such as incorrect data entry, transposed numbers, or forgotten entries. Studies show that 59% of accounting professionals report multiple entry errors per month, often due to multitasking, stress, or tight deadlines.

When financial data is flawed, it can compromise everything from tax returns and audits to internal decision-making. In worst-case scenarios, such errors can trigger penalties or damage investor trust. Automated accounting not only reduces this risk but also provides built-in checks that validate entries before they are finalised.

Inaccurate time tracking

In businesses that still rely on spreadsheets or paper-based time logs, accurate time tracking is nearly impossible. Employees may forget to log hours in real time, miscalculate totals, or even unintentionally exaggerate time spent on tasks. This impacts payroll, client billing, and project profitability.

Further, companies that use manual time-tracking methods are more likely to have billing disputes with clients. It also limits visibility for managers trying to allocate resources or assess performance. This can result in over- or underbilling, disputes with clients, or gaps in internal reporting.

Time-consuming data entry

Data entry requires constant attention to detail, particularly when dealing with hundreds of transactions, receipts, or expense reports each month. Teams often spend hours transferring data from one system to another, matching invoices to payments, or chasing down missing paperwork.

While necessary, these tasks add little strategic value and often compete for time with more complex responsibilities. Over time, this bottleneck can delay reporting cycles and frustrate team members within the finance department.

No real-time data

In traditional accounting setups, financial data is often updated on a weekly or monthly basis, which means that businesses are working with outdated figures. This delay reduces visibility into current cash flow, outstanding liabilities or receivables, and overall financial health.

For companies that need to react quickly due to seasonality, supply chain fluctuations or market changes, this can lead to poorly timed decisions. Forecasts and budgets may be built on assumptions that are already out of date by the time reports are reviewed.

Increased risk of fraud

Fraud risks are higher in environments where there are limited controls or little transparency over who has access to financial records. Duplicate payments, false reimbursements, or unauthorised transactions are more likely to go undetected when oversight depends on manual reviews.

Companies with weaker internal controls report about 50% higher losses compared to those with stronger oversight and automated accounting processes. Beyond financial loss, reputational damage from internal fraud can have lasting consequences with clients and regulators.

Increased costs

While manual accounting may appear budget-friendly, it often comes with hidden costs: higher labour hours, missed deductions, late payments, and the administrative burden of maintaining physical records.

As businesses grow, these costs scale disproportionately and demand more personnel and infrastructure just to maintain basic operations. Errors may also lead to audit issues or missed opportunities for optimisation. This drives up indirect expenses that are difficult to measure but impossible to ignore in the long run.

The main benefits of automated accounting

Beyond reducing basic errors, the transition from manual to automated accounting brings a wide range of operational advantages. Below is an overview of the key benefits and how they contribute to an improved finance function.

Benefits of Automated Accounting

Explanation

Time efficiency

Reduces time spent on repetitive tasks such as invoice entry, reconciliations, and manual reporting.

Accuracy and error reduction

Minimises human input and applies consistent logic to reduce mistakes.

Cost savings

Cuts administrative overheads and improves long-term operational efficiency.

Real-time insights

Offers continuously updated financial data for faster decision-making.

Enhanced security

Protects sensitive data through access controls, encryption, and activity logs.

Tax compliance and reporting

Simplifies regulatory tasks and ensures accurate, timely submissions.

Time efficiency

One of the most immediate advantages of automated accounting is the time it frees up for finance teams. Tasks that would typically take hours, such as reconciling transactions, processing receipts, or generating reports can be completed in minutes with the right tools in place.

Automated workflows further reduce dependency on individuals, and speed up month-end processes. This shift allows finance professionals to reallocate their time toward more analytical or strategic roles.

Accuracy and error reduction

Automated accounting systems apply standardised rules and checks across all entries, which reduces inconsistencies and missed details. Data pulled directly from bank feeds, invoices or payroll systems avoids duplication or manual re-entry errors, while built-in validations flag anomalies immediately before they snowball into larger problems.

Over time, this improves the reliability of financial statements and supports better audit outcomes. Unlike manual systems, automation enforces consistency at scale regardless of transaction volume.

Cost savings

Although automation tools such as expense management software require upfront investment, they yield significant savings over time. Businesses save on labour costs by reducing the need for repetitive tasks and cut down on error-related rework. Improved process efficiency leads to fewer missed deadlines and reduced reliance on third-party accountants or consultants.

Additionally, the ability to detect and prevent financial leakages such as duplicate payments or unclaimed tax deductions can have a measurable effect on the bottom line. These savings are especially meaningful for SMEs with limited resources.

Real-time insights

Access to up-to-date financial data allows companies to react quickly to internal and external developments. Automated accounting continuously syncs with bank accounts, expense apps, and payment platforms. As such, companies gain instant visibility into cash flow, outstanding invoices, and operational costs.

Real-time dashboards make it easier for managers and business owners to track KPIs and identify trends before they escalate. This constant flow of information supports strategic decision-making and provides a competitive edge in fast-moving markets.

Enhanced security

Modern accounting platforms are equipped with advanced security features that go far beyond password protection. These include role-based access controls, two-factor authentication, and activity logs that show exactly who made which changes and when.

Sensitive financial data is secured with encrypted protocols and backed up in the cloud to protect against data loss or unauthorised access. For businesses handling payroll, tax documents or client invoices, this added layer of security also helps meet data protection regulations and build trust among customers.

Keeping up with tax regulations can be daunting, especially as rules evolve. Automated accounting systems are often updated in real time to reflect changes in tax law, which helps businesses remain compliant without needing constant manual oversight.

They also generate standardised reports such as VAT summaries, profit and loss statements, or expense breakdowns to simplify filing returns. Audit trails and document storage solutions further facilitate the necessary paperwork during audits or reviews.

How AI is changing automated accounting

AI is accelerating the shift from manual accounting to intelligent workflows.

Instead of manually entering data:

Invoices are automatically read and processed

Payments are prepared automatically

Transactions are matched in real time

This allows finance teams to focus less on data entry and more on decision-making.

Team expenses used to be Excel only. Now it’s just automated. My accountant says we save at least 10 hours per week.

Lennart Rieper

Managing Director, STRYVE

Automate accounting processes with amnis

amnis’ financial ecosystem helps companies automate accounting processes while reducing international transaction costs.

With amnis AI & Automation, routine financial tasks are prepared automatically – from invoice processing to payment creation and transaction matching. You stay in control at every step, reviewing and approving what gets executed.

Multi-currency accounts and cards simplify global finance operations. You manage payments, expenses, and balances across currencies from a single platform and login – without switching systems or duplicating work.

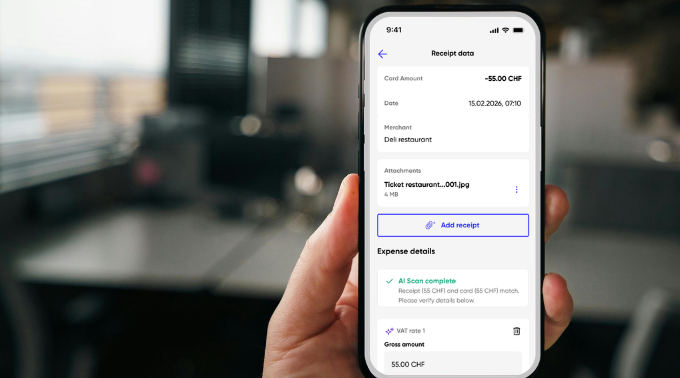

With features like Expense AI, receipts are automatically captured, matched to transactions, and pre-categorised – including VAT extraction and cost centre allocation. At the same time, integrations with your accounting tools ensure that data flows seamlessly into your existing setup.

The result: less manual work, lower costs, and consistent, audit-ready financial data.

What you can automate with amnis:

AI-powered invoice and receipt processing (Expense AI)

Automated payment preparation and approval workflows

Multi-currency accounts and debit cards in one platform

Auto-accounting for transactions, expenses, and recurring activities

Third-party apps such as H2H (SFTP), Exact Online, bexio integration & more.

24/7 access to all financial data from a single dashboard

As Senior Content Writer at amnis, Elena transforms complex financial and banking topics into clear, insightful content for SMEs. She focuses on areas such as the FX market, international payments, cross-border business operations, and regulatory updates - ensuring companies have access to reliable and easy-to-understand guidance.

With a strong background in research and communication, Elena plays a key role in helping businesses stay informed, make smarter decisions, and navigate the evolving world of international finance.

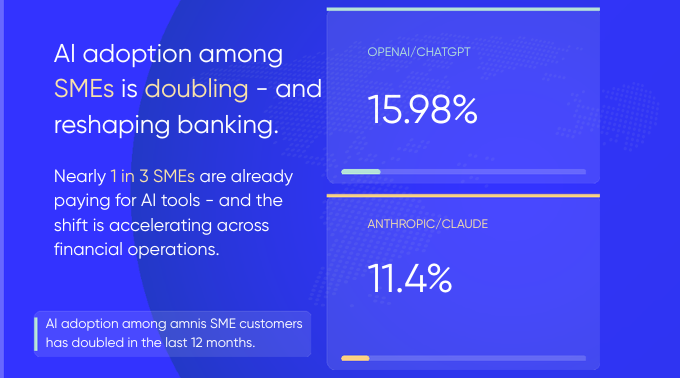

Nearly 1 in 3 amnis SME customers is paying for a leading AI platform. AI adoption among SMEs has doubled in 12 months — here's what the data shows and what we're building in response.

Companies face growing risks of fraud, data breaches, and overspending without proper financial controls, especially in digital-first environments. Find out how temporary credit cards offer a simple, yet effective solution to provide enhanced security, spending limits, and real-time tracking. Common expense management…

Stay updated

Get the newest insights, expert tips, and research findings delivered straight to your inbox, so you never miss a beat in the industry.